May Stock Update

Closed

Sirius XM (SIRI)

Everything was going fine – until a rumor hit the newswire that Sirius XM may acquire iHeartMedia (IHRT). There's a whole history between the two.

The short version is Sirius and XM merged in 2008. In 2009, John Malone and Liberty Media saved Sirius XM by investing $530MM in loans and convertible preferred stock, giving Liberty a 40% convertible interest in the company.

By 2013, Liberty Media owned over half of Sirius XM.

At the same time Sirius and XM were getting married, iHeartMedia (previously Clear Channel Communications) was being LBO'd by Bain Capital for around $18B.

By 2018, iHeartMedia filed for Chapter 11. The outdoor advertising business (Clear Channel Outdoor) did not file with it. iHeart negotiated for creditors to cut the debt from $16.1B to $5.8B.

During the restructuring, Liberty bought $600MM face value IHRT debt for $490MM, which converted into almost 7MM shares, which Liberty eventually sold.

Liberty and Sirius XM separated in 2024. And here we are.

Now Sirius XM is supposedly in preliminary talks to acquire/merge with iHeartMedia.

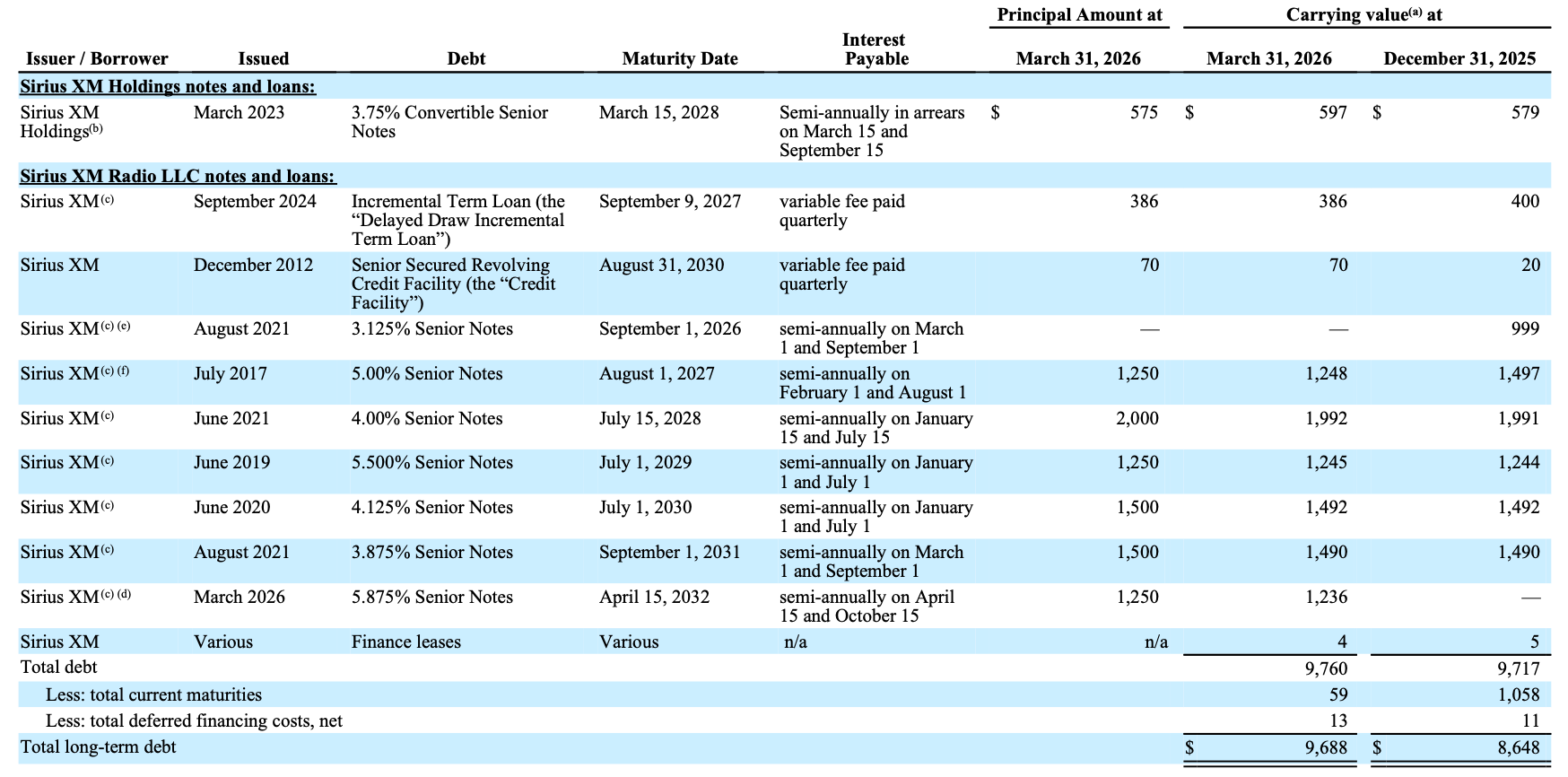

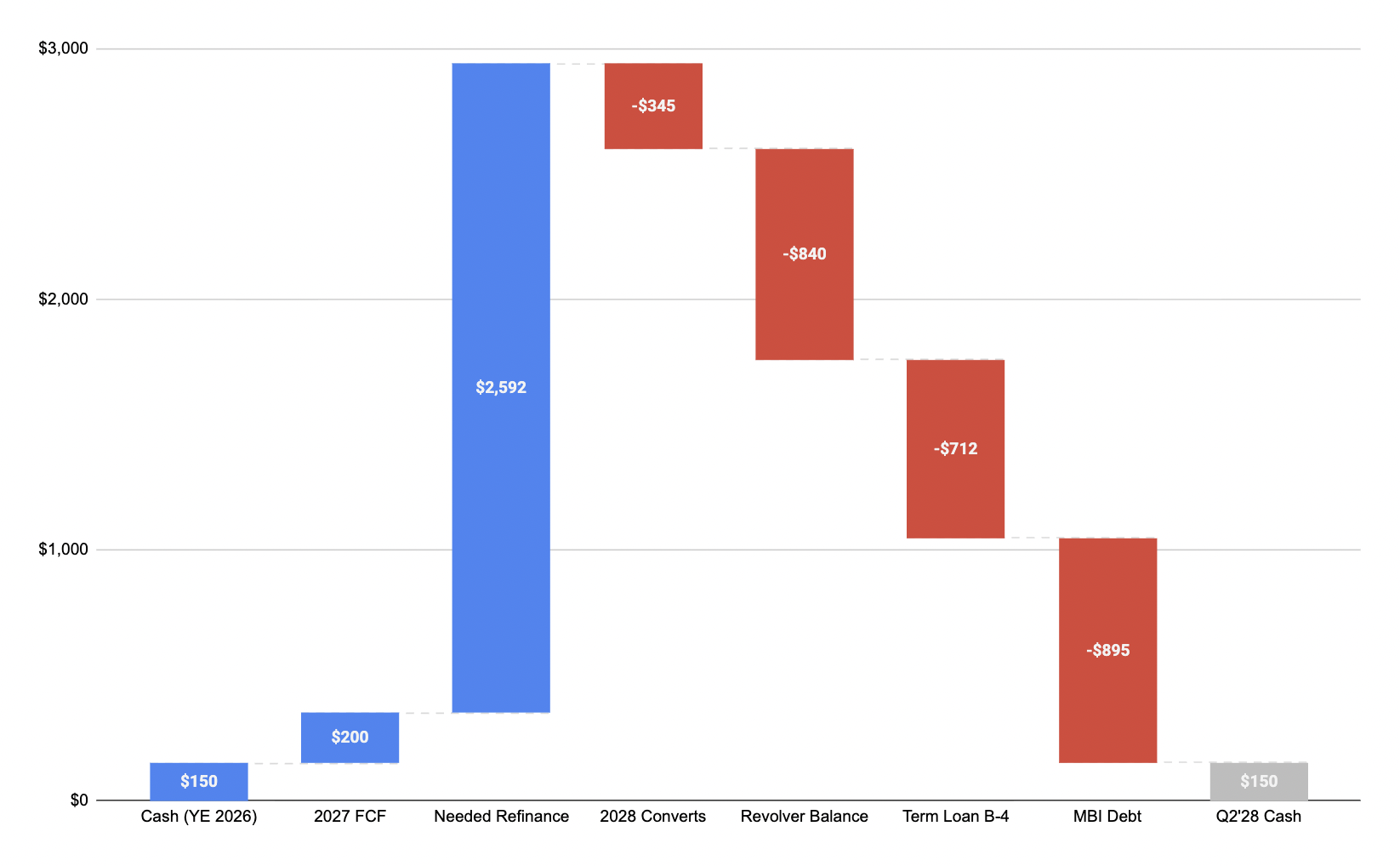

The problem for me is Sirius XM has a wall of maturities over the coming years.

For a company heading towards $1.5B FCF, that's manageable. Pay some, roll some. I was willing to delay gratification of any buybacks etc for a few years while they deleveraged.

$9.5B market cap + $10B net debt and doing $1.2-1.5B FCF. Not bad.

iHeart on the other hand is $900MM market cap + $4.5B net debt doing $200MM FCF – at least that's 2026 guidance. And they include real estate sales in their FCF calculation.

For FY2025, IHRT did $11MM FCF. If you include real estate sales, $31MM.

So, a much more financially sound and profitable company trading at 13x EV/FCF wants to acquire a company constantly on the verge of bankruptcy and renegotiating with creditors for 27x a very generous definition of 2026 FCF.

SIRI does ~$2.7B EBITDA. IHRT does $800MM.

Almost all of iHeart's debt matures in 2029 ($2.8B) and 2030 ($1.3B).

Maybe SIRI gets good terms on the deal. But if they decide to go through with the acquisition, safe bet it's going to involve issuing shares.

Dilution in return for more debt and a turnaround story isn't my idea of a good time.

Liberty management, when asked for their plans with their iHeartMedia stake after the restructuring, said they would wait and see how it performed. Eventually they sold and are now interested again at half the price before ("they" being SIRI).

Maybe I'll get the same opportunity down the road.

Entry (first wrote about): $20.90

Exit (price at last close): $26.68

Return (including dividends): 29% vs 9% SPY

Results for stocks I write about or mention are listed at the page below as a sort of scoreboard.

DaVita Inc (DVA)

DaVita stock increased enough that it's closer to what I think it's worth than not, so I closed. It's volatile enough that I expect it won't be the last time I own it. It wasn't the first.

Entry: $142

Exit: $193.88

Return: 37% vs 7% SPY

Updates

Cable One (CABO)

Just two weeks ago I said "Still ugly. Still Interesting. Still Waiting."

Well, recent earnings were ugly. It's less interesting. But I'm still waiting – reluctantly.

Lone Elm Capital recently published an update and disclosed that they've closed their position.

Understandable.

Things are melting quickly, and I have no real reason to own it aside from hoping someone acquires it. My only guess for why I don't sell is it's such a small position (and getting smaller by the day) and I'm curious to see what happens.

Omnicom (OMC)

None of the above positions really matter when 75% of my portfolio is in Omnicom.

Pre acquisition, OMC was generating $1.5B FCF and IPG $1B.

That equals $2.5B combined. Subtract maybe $120MM from divestitures and you're left with $2.38B run rate.

2026(e) cost synergies are $900MM. Cost to get them is estimated at $250MM. Assume 60% of the $650MM savings drops to bottom line (FCF) and that's $390MM on top of $2,380.

Shares outstanding within 12 months would be around 256.6MM (assuming current stock price holds). That brings 2026 FCF to $10.80 per share. Closing price today was around $77.

You can also take the combined OMC + IPG Adj. EBITDA reported in the 2025 OMC presentation of $4.06B and back out ITDA — leaving ~$2.44B FCF.

Or read the S-4 where they have (un)levered FCF estimates (higher estimates than we’re using here).

Or start at $23.1B combined revenue estimate net of planned dispositions they had in their presentation. Slap a 15% EBITDA margin on it.

= $3.465B EBITDA - $392.7MM D&A (1.7% of rev) = $3.07B - $235MM interest expense = $2.837B * 26% effective tax rate = $2.1B excluding synergies.

OMC 2028(e) FCF is likely $3-3.28B

@ 236.5MM s/o (assumes another 10% buyback this year (stated / around current prices) and then 4% in 2027 and 2028) and OMC is trading at 5.5-6x 2028 FCF.

What happens if none of the synergies are realized? It's trading around 10x FCF. What happens if they get the synergies but face pricing pressures from AI or economic softness and marketing cuts? They're trading somewhere between 6-10x FCF.

All to say, a lot is going to have to go wrong before things get concerning from a permanent loss of capital perspective.

They're borrowing at 5% to buy back stock paying a 4% dividend. Considering tax effects of higher interest expense which lowers taxable income, the cost is minimal and they're getting a hell of a valuation. They could buy back 1/5 of the company at 5-7x 2028 FCF in the span of 15 months. They already bought back 10% in 3mo.

So, yes, this feels like one of those situations not to hold back on. Nobody cares. I don't think anyone is paying attention. Hardly anyone seems to actually understand what they do. I feel good.

Member discussion