April 2026 Stock Updates

Closed

TD SYNNEX (SNX)

SNX reached my range of fair value, so I closed it. If it's anything like Ecovyst, it'll keep going up. But, it's close enough to my upper bound of $230 that I'd rather reallocate to something else.

They had a great 1Q FY26. And, after initially traded down, has been on quite a run. It's still a good business and one I keep a close eye on. I like the business and it's a volatile stock. It just moved from attractive to fair.

Writeup was here:

Entry (first wrote about): $159.03

Exit (price at last close): $214.32

Return (including dividends): 35.1% vs 3.2% SPY

Results for stocks I write about or mention are listed at the page below as a sort of scoreboard.

Open - Updates

Omnicom (OMC) / Publicis Groupe (PUB.PA)

Still my largest positions.

We call them advertising companies, but majority of their business is distribution and data analytics. The traditional mad men advertising business people think of is less than 20% of Omnicom's business.

With the IPG acquisition, Omnicom now controls over $70 billion in advertising budget. A company which sells its products in countries across all continents, cultures, languages etc is always going to use a distributor like Omnicom or Publicis who has local networks who understand local nuances to distribute that budget.

Businesses like Google, Amazon etc. are isolated silos. Google has a great ad business and valuable set of data. But it's isolated. They're never going to share their data with Meta. Meta won't share their data with Amazon. But an advertising agency like Omnicom sits above all that and distributes marketing spend across Google, Meta, social media, TV, newspapers, radio etc., collecting all that data in the process.

It is why Google, Meta and AI will likely never replace the advertising agencies. In fact, although they compete to a degree, the former likes the latter because the advertising agencies brings them business.

And, if there's any validity to SaaS becoming commoditized and data all-valuable, guess who has some of the most valuable data on people? Omnicom's recent acquisition of Acxiom Real iD gives them specific data points on 98% of all people inside the United States – not just at the household level but at an individual level. Over 2.6 billion people globally.

All of this, worst case scenario, trading at 10x FCF. More likely 7-8x. And there's a non-zero chance OMC is trading at ~5.5x three-years-out FCF. Managements expected synergies target doubled from $750MM to $1,500MM after the IPG acquisition closed.

I think it's worth twice where it's currently trading. And it's why 75%+ of my portfolio is in it.

OMC

Entry Price (first wrote about): $80

Current Share Price: $79

Price Target: $100 to $180+

Upside (downside): +27% to +127%

Publicis is a better company, but in terms of valuation has less upside than OMC. Publicis 2026-28 management guidance is confident in at least 4% top line growth, 7-9% EPS growth per annum + 5% current dividend. That's 12-14% expected annual return excluding multiple expansion (or contraction). Currently trades at less than 9x FCF.

PUB.PA

Entry Price (first wrote about): €77

Current Share Price: €80

Price Target: €121.50

Upside (downside): +50%

Ardent Health (ARDT)

Ardent did $170MM FCF in 2025 against my original normalized estimate of $190MM. Guidance for 2026 is higher revenue, lower EBITDA. Normalized FCF is probably closer to $150MM, but if I assume $100MM I still get a fair value on ARDT of around $11 per share vs $8.55 cost and ~$10 current stock price.

I still think it's worth closer to $16, and if margins normalize higher then I'm back to my original $17-20 range.

All that to say, 1) I seemed to have been off the mark on FCF, but 2) the range of outcomes is still higher above where it's trading. The big question mark is what they plan to do with all the cash on their balance sheet.

Entry Price (first wrote about): $9

Current Share Price: $10

Price Target: $16-20

Upside (downside): +60% to +100%

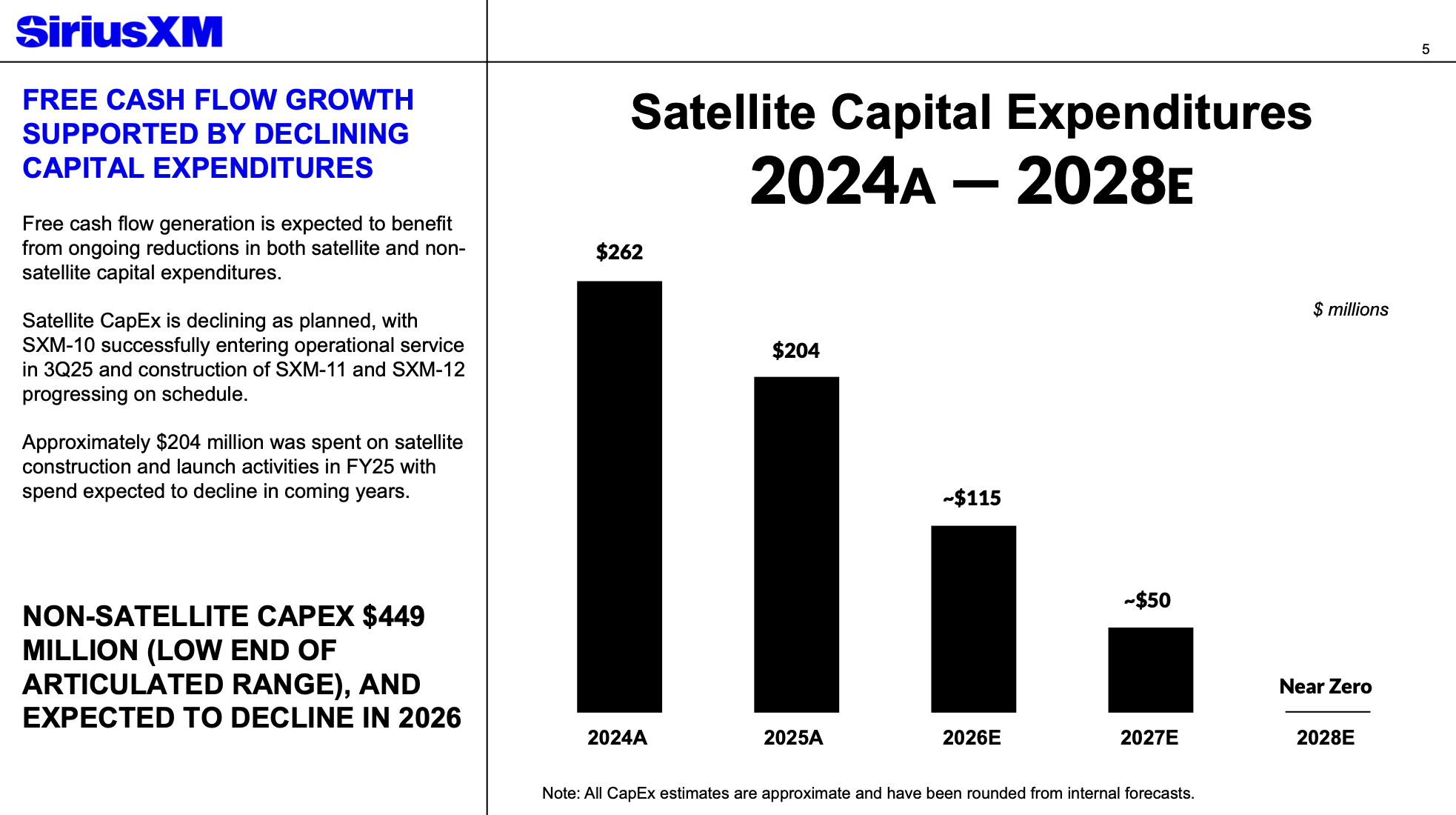

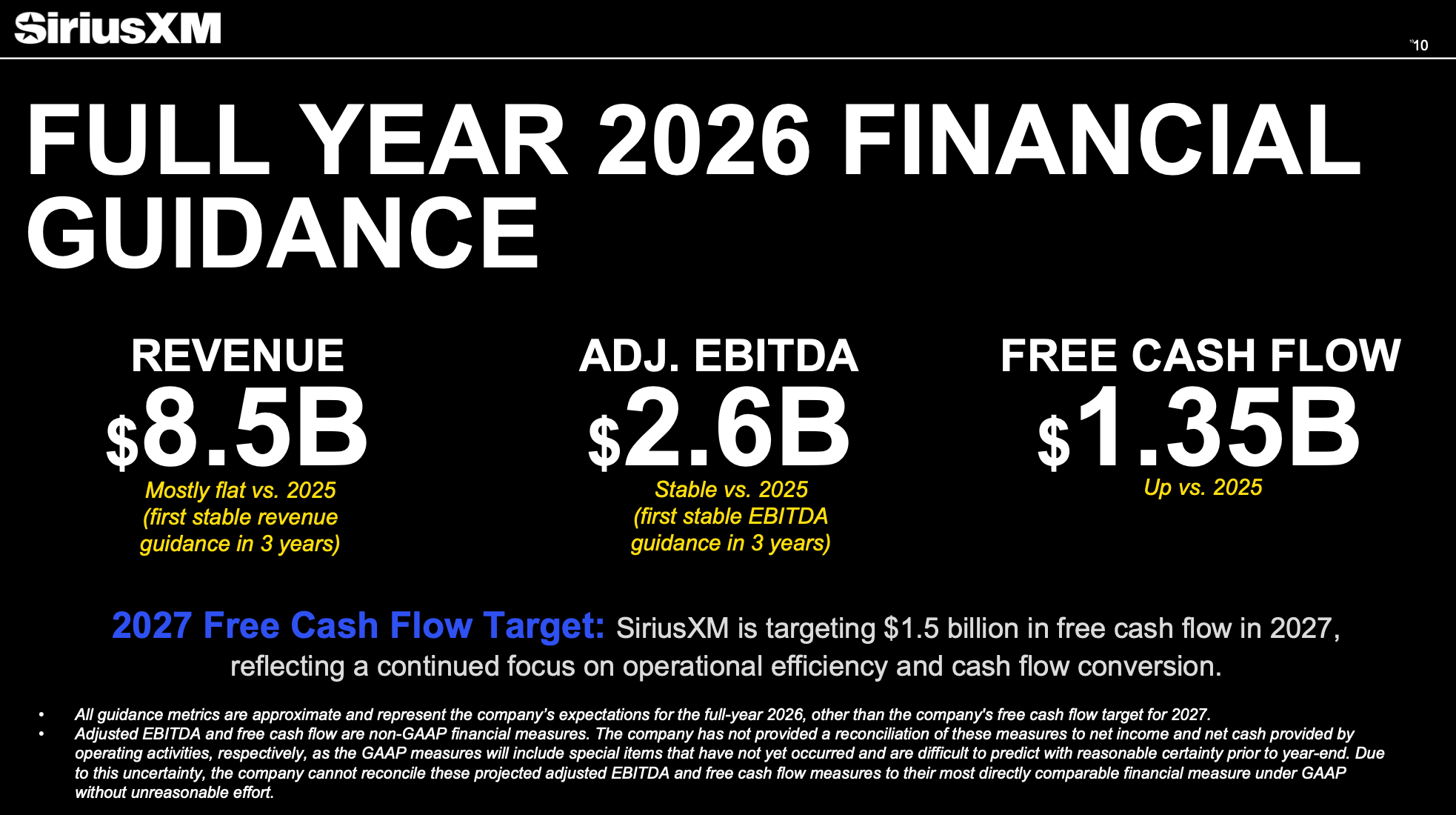

SiriusXM (SIRI)

The thesis is unchanged. Capex down, FCF up. It keeps playing out and people keep saying it won't happen (Elmo shrug).

2024 FCF: $1,015MM

2025: $1,256MM

2026 (guidance): $1,350MM

2027 (target): $1,500MM

Since 2024, people have been telling me it's a melting ice cube and they wouldn't grow FCF let alone hit the $1.5B target.

I don't know how people math but seemed like a good bet to me – it relies mostly on spending less which is completely in management's control.

SIRI chart looks good and the stock hit a new 52 week high last week.

Entry Price (first wrote about): $21

Current Share Price: $25.50

Price Target: $15 to $65

Upside (downside): (-40%) to +155%

Cable One (CABO)

Still ugly. Still interesting. Still waiting.

Lone elm has done great work on it so I'm not about to reinvent the wheel.

Entry Price (first wrote about): $101

Current Share Price: $107.50

Price Target: $120 to $380

Upside (downside): 10% to 250%

DaVita Inc (DVA)

Sticky business generating $1B free cash flow. Mid-point 2026 FCF guidance is $16.40 per share. Buying back stock.

Risk: dialysis becomes a political piñata / reimbursement rates.

Entry Price (first wrote about): $142

Current Share Price: $148

Price Target: $225

Upside (downside): +50%

Conagra Brands (CAG)

Conagra has been a dog. On the other hand, organic sales were up in 3Q FY26 and they're getting a new CEO. Dividend yield is approaching 9.5% which is covered (for now).

Entry Price (first wrote about): $20

Current Share Price: $15

Price Target: $12 to $25

Upside (downside): (-20%) to +67%

Open - New

Wendy's (WEN) - Jan. 21, 2028 $10 Calls

The food tastes like the chart looks – not good. But there is cash flow; on the other hand, leverage. One of those situations that I should pass on but think there could be value. Small options position scratches the itch.

Shorts - New

I haven't written about shorts before. They're usually small positions I do for the love of the game.

Millennial Potash Corp (MLP.V)

MLP.V is a Canadian listed American gold turned African potash project with a USD $1,071MM estimated post-tax NPV, market cap of USD $165MM, initial capex estimate of USD $480MM, $30MM cash, and incomplete feasibility study. The stock is up 800% in the last two years. The project, if completed, will take a lot longer than that.

Abacus Global Management (ABX)

No comment.

DHT Holdings (DHT)

I love shipping, but at this point in the cycle the best outcome is another double from DHT. Not the type of R/R I'd want to play for in shipping.

Everyone knows how much cash they're printing right now. And bulls are excited for dividends. But, if DHT were to pay $2 per share dividend each year for the next 3-4 years, at which point the cycle is over and the stock goes to $6 (and probably lower than that), why would you expect it to trade any higher than it currently is today other than that's what you (bulls) want, or speculation?

By the time shipping companies are trading at low P/E ratios with clean balance sheets, you're at least half way through the cycle. Newbuilds are coming in and the market is forward looking.

There may be some more upside or quick trade, but my guess is this run is closer to the end than the beginning.

Closing Thoughts

Someone tweeted a good clip from Greenblatt's Columbia lecture notes recently:

...what I am always doing is valuing the company when I can. What happens if it is very difficult to value a company? Do something else. That is a very powerful concept if you have the luxury of looking at something else. The guarantee I made last week is that if your valuation is right, it will usually only take Mr. Market two or three years at most—sometimes a lot faster--to get it right. Do good valuation work.

That's basically how I think about investing.

I do not believe I have some magic edge. I do think I am decent at valuing businesses, or at least being conservative enough that I'm usually right more often than I'm wrong.

Most of the companies I get involved with I've followed for years. Occasionally they get cheap relative to some range of values I think they're worth. It's been my experience that, like Greenblatt said, the market usually converges on that in 2-3 years at most, and more often 1-2.

As always, none of this is financial advice. Just me jotting some notes on what I'm doing.

Member discussion